Managing Cashflow

Cashflow represents the net amount of cash and cash equivalents moving in and out of a company. One of the most important resources is their ability to continue its operations by generating sufficient in and out cash and cash equivalents.

In simple terms, cash received represents inflows, money spent represents outflows.

This creates questions around the management of cashflow:

How do they use cash?

How does it generate cash?

What are the expectations of paying a cash dividend?

Will they satisfy its upcoming interest and loan obligations?

Considering the above, the financial statement of cashflows provides users a summary of the inflows and outflows, while allowing users to understand the how and why cash has changed over a period. This becomes important to reviewing a company’s ability to create value, generate positive cash flows, and take advantage of long-term free cashflow.

Benefits of cashflow information

To evaluate the changes in net assets

Provides an overview of a business’ financial structure - solvency and liquidity

Allows a business to easily adapt to changing circumstances and opportunities

Cash Flow vs Profit

It is important to remember there is a clear distinction between making a profit and generating cash flow. Profit is revenue minus expenses paid, while cash flow is the cash remaining after meeting obligations.

Types of Cash Flow

Operating Activities- Principal Revenue-Producing:

Operating activities are an indication of whether an entity has generated sufficient cashflows to repay loans, maintain the operating capability, pay dividends or make new investments without external financing.

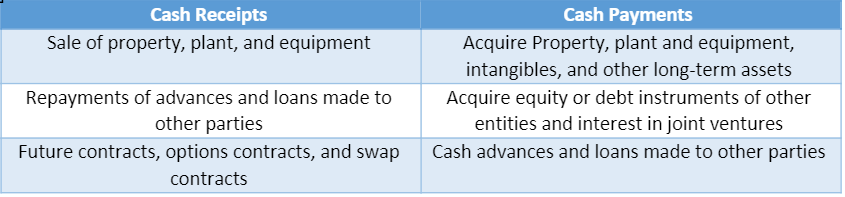

Examples of cash receipts and cash payments related to operating activities.

Investing Activities - Resources intended to generate future income and cash flows:

Investing activities are expenditures that result in a recognised asset.

Examples of cash receipts and cash payments relating to investing activities.

Financing Activities: Debt/Equity Instruments

Financing activities are debt/equity instruments that are useful in predicting claims on future cash flows as they are providers of capital to the entity.

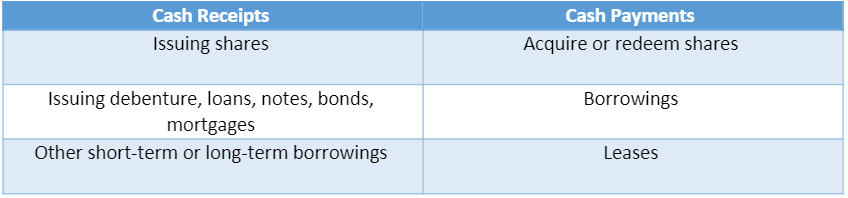

Examples of cash receipts and cash payments relating to financing activities.

Analysing Cash Flows

By understanding the information provided in the financial statement of cashflows, we can start to analyse and forecast an entity’s future financial position. The metrics we use are as follows:

Free Cash Flow (FCF)

FCF indicates the company’s ability to generate cash to use for expansion, improve operations, repayment of debt and increase return to shareholders.

FREE CASH FLOW = OPERATING CASH FLOW - CAPITAL EXPENDITURE

Debt Service Coverage Ratio (DSCR)

This will assess the ability to meet principal and interest repayments in a period. When the result reflects less than one, it indicates there isn’t enough net inflow to cover the minimum debt repayments.

DEBT SERVICE COVER RATIO = NET OPERATING INCOME / SHORT-TERM DEBT OBLIGATIONS

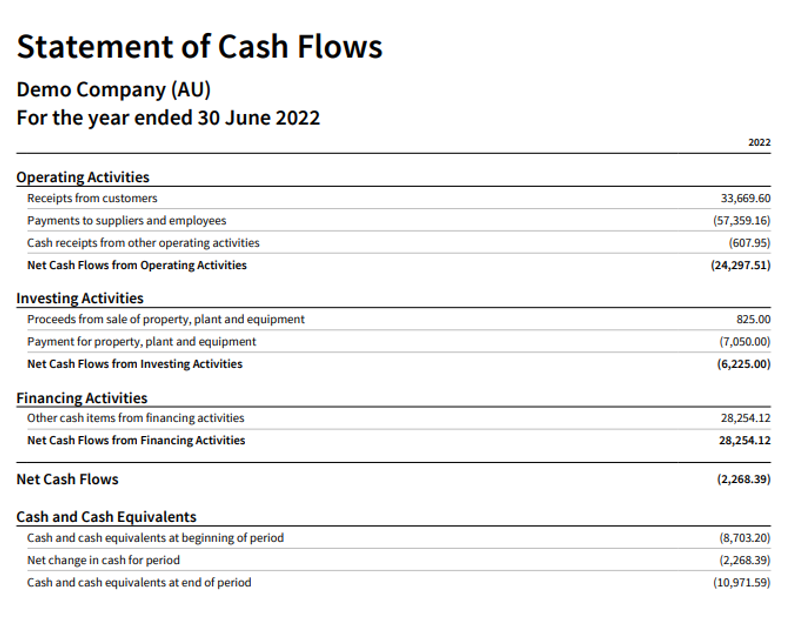

Basic Example Extracted from a Demo Company in Xero

Managing your cashflow allows you to have a clear overview of the company and allows you to make business decisions that can help the company grow.

Cashflow forecasting can assist with this. By estimating the future income and expenses, you will be able to project if you have enough cash to run the company, or if it can be expanded and grow.

For more information and assistance, speak to your Kamper accountant.